To the non-existent visitors, am moving to the new add given below. The reason for moving is the atrocious formatting and word document settings of Blogspot. This is not to say that 'posterous' [the new site] is brilliant, but it allows me to put up my .doc files as is, without being fussy about footnotes and bulleting- and i love my bulleting. Will be putting up new [and old] material on the new site and hope you are more interactive in future.

- Mike.

New address: http://thenativeopinion.posterous.com/

Sunday, July 17, 2011

An economic rant [in more ways than one] :)

Assumption: There exists a “disconnect” between the markets and reality with regard to valuation and methods to determine the same. Also assume that we are all rational investors.

A simple and oft repeated maxim for a retail individual is “buy low, sell high”. Investment theory, macro-micro economic policy everything else is white noise for a middle class retail investor. Now reflect how many times you actually followed this maxim. As with everything else in life, practical application is the greatest challenge. It is very difficult to follow the maxim when the neighbours are all either panicking or in euphoria. Going with the herd is as strong an instinct as life-preservation, but a great deal more subtle.

Look at the present situation, the domestic market we see today is on the last legs of the “mispricing” of risk phenomena, that has been the life of the party for more than a decade. Institutions “mispriced” the risk of perverse incentives, macro-economic policy wonks mispriced the importance of achieving a stable inflation rate, loan officers “mispriced” the cost of giving loans to high credit risk clients, bankers “mispriced” the cost of packaging and leveraging risky products and rating agencies “mispriced” the cost of closing their eyes to everything.

Now lets agree that we all got sucked in by the aggressive expansion of the last decade. Truth be told we are still reluctant to give up this story. The present situation is pretty muddled and for a retail individual extremely confusing. Especially so as the present market rally has come on the heels of a sobering shock. Look around, the BSE and NSE are hovering within sniffing distance of their pre-2008 highs along with high growth for gold, silver, oil. Throw in a few scares like the rare earth shortage, fear of sovereign default contagion spreading through EU, political instability throughout the middle-east, food price inflationary shocks, natural disasters and we have got a tinderbox primed and ready- or at least feels like one. The market is currently living out its half-life moment.

The prime market of the world, United State of America is presently involved in papering over its shot up economic engine by monetising its GDP. The ill-effects have been out-sourced to the world, such is the price we pay for the “reserve currency”. Credit expansion with low policy rates and sustained high liquidity has been the default policy and the same is being rolled out on a world wide scale in an attempt to ride out this storm. For the politicians and policy makers such short term strategies make sense especially in a democratic set-up where the costs will be borne by the next government.

The present uncertainty is not just a regular event in the economic model, but a result of limitation of the model. It is imperative that the economic model of sustained high growth, low interest rates, high and continuous liquidity with large resource utilisation be discarded. In the meanwhile, the retail investor will continue to be taken for a ride on the wildest roller coaster in the world.

Friday, June 24, 2011

Thoughts

I had put an article on the UNCRPD and thoughts on the same yesterday (the Hindu incidentally stole this theme, apropos the editorial today); bad coding of the word processing (if it can even be called that) on BlogSpot saw to it that I inadvertently destroyed the formatting completely. Having been on the blog for a short while, I now see two types of postings; well have seen only one but I mean space for two types: Short articles, like the opinion-editorial pieces which come within a page or five and then the plodding articles and regurgitated minutiae like what I have put up running into 8-15 pages, and then there is the third type which is the twitter-facebook-gtalk status updates (of which the less said the better- possible motto there eh.....!). A reason for twitter-facebook-gtalk popularity is because the vast majority of us have nothing much to say, and those who do either have a willing audience to impose on or the wherewithal and means to enthral an un-willing one. This leaves misanthropes like me, who have the need and information to say something, but cannot be bothered to interact with humanity long enough to say their piece.

- Mike

Saturday, May 28, 2011

Turbomeca-HAL dispute.

The news and discussion on Turbomeca-HAL dispute on provision of Shakti engines for LUH; set me off on thinking on what would be the commonality of engines for Helicopters for the Largest users and producers of Helis viz., USA and Russia. Accordingly have collected the information on an excel sheet.

If we see the US numbers we can see that only 4-5 powerplants have been repeated across a minimum of 19 helicopters. A number of platforms have been excluded as being variants of the same platform. A similar case is seen with the Russian helicopters. Here my information is severely lacking and the conclusions might be wrong. However it might be safe to assume that commonality of engine across platforms is not a compulsory best practice.

Though the benefits of commonality are obvious, it might be more important to find an engine which is more suited to the need of the platform.

Sunday, May 8, 2011

Hello.

So, have been remiss in missing my self imposed deadlines. However in the interest of furthering my 10000 project, will do the needful this week, pakka. The topics that will be covered are (tentative list):

1. Foreign Policy for India 2nd post.

2. Preliminary analysis for US Senate data; raw dump for which is already put up.

3. A jab at discussing the defence industry development in Korea and Israel, which this author thinks are the closest parallels for Indian Defence Industry. More to the point, why the clamour for increase in FDI in Defence may be a case of barking up the wrong tree.

Well that should make it a busy week.

I discovered a new feature in the settings section, called "Stats". It is not 'new', but new in the sense of newly discovered. Now i thought that no body had read this blog as of yet, and was pleasantly surprised to know that the visitors numbered in the low three figures, but then again that might be just me visiting this page. Further i realised that there were a few visitors from the Russian Republic. Now seriously that warms the cockles of my shriveled heart. So here is a shout out to the mystery Russian visitor or visitors: "Hello".

Also could you, please tell me what brought you to this blog. It would genuinely help in boosting my ego :).

1. Foreign Policy for India 2nd post.

2. Preliminary analysis for US Senate data; raw dump for which is already put up.

3. A jab at discussing the defence industry development in Korea and Israel, which this author thinks are the closest parallels for Indian Defence Industry. More to the point, why the clamour for increase in FDI in Defence may be a case of barking up the wrong tree.

Well that should make it a busy week.

I discovered a new feature in the settings section, called "Stats". It is not 'new', but new in the sense of newly discovered. Now i thought that no body had read this blog as of yet, and was pleasantly surprised to know that the visitors numbered in the low three figures, but then again that might be just me visiting this page. Further i realised that there were a few visitors from the Russian Republic. Now seriously that warms the cockles of my shriveled heart. So here is a shout out to the mystery Russian visitor or visitors: "Hello".

Also could you, please tell me what brought you to this blog. It would genuinely help in boosting my ego :).

Tuesday, April 12, 2011

Attempt to quantify political background of the US Senate

This note was triggered by an article of ‘Patrick French’ which looked at the composition of the Lok Sabha and came to the conclusion that a significant minority of the Members of Parliament [henceforth MP(s)] had political family backgrounds. According to this study the breakup was as follows (descending order)[1]:

1 | No significant family background | 46.8 |

2 | With family background | 28.6 |

3 | Student politics | 8.6 |

4 | Business | 6.4 |

5 | Others | 9.6 |

All number in percentages.

Mr French also provides numbers for the political back ground of the “gen next” Lok Sabha members. These numbers are quite intriguing. According to Mr French’s analysis, the majority of MP (Lok Sabha) seats are earned so to speak, with a significant minority being cornered by the politically influential. What is significant here is that an overwhelming majority of the gen next politicos are from political families, with many winning from regions which have been loyal to their family for at least a generation. These seats might be considered a version of the English phenomenon of ‘Pocket Burroughs’.

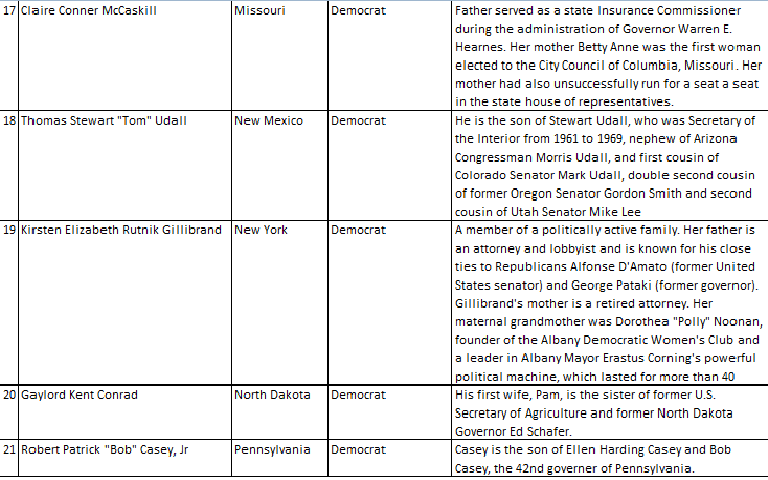

I am not writing this post to actually comment on this article, nor to bemoan the alleged decay in Indian democracy. My main purpose is to see if I can do a similar analysis, with collection, sorting of information and analysis of trends. To this effect, I have chosen to do a comparative analysis of the political backgrounds of the 116th United States Senate. The US Senate was chosen to fulfil twin objectives of gaining experience in analysis and to put the Lok Sabha numbers in perspective by creating a counterpoint. Let me clarify that as I wanted to see how I would fare in my first attempt, I have not looked at the numbers, research methodology or information sorting system employed by Mr French. This would be done after the first attempt.

I am compiling information on the senate members, with information sourced from the open source web. The initial list will only contain information on senators that have politically backgrounds in my opinion. I would here like to explain my under-construction understanding of “Political Background”. As has been mentioned before, the definitions and methods employed by Mr French have not been looked at, except a cursory look at his article. A general online search does not provide a definition of “political background” which would be independent of regional context. An attempt at defining political background is fraught with pitfalls as more often than not it might include self-made individuals who might be part of popular families or might exclude individuals who are politically strong but are not in the public eye.

I believe that irrespective of individual capabilities the power of ‘linkages’ helps in tangible means, albeit ones which do not lend themselves to 2 paragraph descriptions on ‘Wikipedia’. This is one of the larger challenges for a researcher that is lack of a local context. The category for defining a senator as one having ‘political background’ is to confirm the senator has someone in the family who is or has held political posts in the government. As I have chosen to give importance to the power of linkages i have also included family members who hold or have held posts in the military or diplomatic corps especially if these posts were held at significant moments of national history.

Examples are the reefs on which many a definition founders. Especially if the definition is an tenuous as the one above. I have sought to place importance on strong hereditary political influence. This however is inadequate in categorizing individuals who have attended schools with future leaders; or if an individual’s close relations marry into a political family; or if only the first wife was from a political background.

The list of Senators with political backgrounds is being provided below:

[I have to attach the documents as .png format as Blogspot does not allow excel to be incorporated into the post.]

Analysis should come up this weekend.

[1] http://www.outlookindia.com/article.aspx?269931; http://pragmatic.nationalinterest.in/2011/03/20/on-hereditary-politics/

Sunday, February 6, 2011

Why claims of RBI to regulate NBFC (MFIs) is > Federal state govt claims. An analysis of constitutional provisions.

This article was first posted on the "IFMR Blog". Am cross posting it here.

A verdict on the Malegam committee reports efficaciousness is still out. However there is a consensus arising about the benefits of a few suggestions. One of these being, if the recommendations of the Malegam report are accepted, the need for a separate Andhra Pradesh Micro Finance Institutions (Regulation of Money Lending) Act (henceforth the Act) will not survive.[1]

The AP state government has responded to the report in general and this recommendation in particular with dour criticism and expression of support for its legislation. Further the AP government is claiming the protection and empowering cloak of the Indian constitution for the continuance of its Act. Rural development principal secretary R Subrahmanyam was cited in a news report claiming:

“According to the List II of the Constitution, the regulation of money lending is the original jurisdiction of the state government. An Act is the will of the people. Accordingly, whether or not the need for AP MFI (Regulation of Money Lending) Act exists will be decided only by the AP Legislature and not by the RBI”.[2]

Other criticisms were levelled at the report which was submitted to the RBI in a 5 page report, excerpts of which can be found in the public domain[3]. However for the purpose of this article we will focus only on the above statement, whereby state government regulation is given primacy over central regulation.

The constitutional powers debate:

The primary issue in our context is one of jurisdiction. Is regulation by federal units of India valid if a class of institutions are already under the purview of ‘central watchdogs’.

The primary argument utilised by the AP govt deals with the concept of separation of powers which is enshrined by the Indian constitution via Article 246. This article combined with Schedule VII lists the areas which are the exclusive domains of the Centre, the State and common areas of interest.

Under List I which lists central government’s sphere of responsibility the following entries are relevant:

Entry 38: Reserve Bank of India.

Entry 43: Incorporation, regulation and winding up of trading corporations including banking, insurance and financial corporations but not including co-operative societies.

Entry 44: Incorporation, regulation and winding up of corporations, whether trading or not, with objects not confined to one State, but not including universities.

Under List II which lists state government’s sphere of responsibility the following entries are relevant:

Entry 30: Money-lending and money-lenders; relief of agricultural indebtedness.

Entry 32: Incorporation, regulation and winding up of corporations, other than those specified in List I, and universities; incorporated trading, literary, scientific, religious and other societies and associations; co-operative societies.

The Rural development principal secretary R Subrahmanyam is depending on entry 30 List II cited above to derive sustenance for the Act. A preliminary reading of the above entries leads us to see AP government’s Act as a case of constitutional over reach; especially when the act seeks to infringe onto RBI’s turf. The entries and hence the constitution is clear that the state government can only regulate those financial corporations which are not regulated by the central govt. Further the RBI is under the exclusive control of central regulation. Money lending under entry 30 list II cannot be given such a wide interpretation so as to encompass areas under exclusive central regulation and thus defeat the language and spirit of the constitution.

If we assume the above argument to be valid, RBI and its regulatory powers are derived from List I and will be equivalent to central government regulation. Thus in the present context we are dealing with over-regulation of NBFCs’ by state and central laws.

With the insertion of chapter IIIB in the RBI act, it has become compulsory for NBFCs to register with the RBI, which has specified various restrictions in the context of income recognition, asset classification, capital adequacy norm, provisioning requirements and disclosures in the balance sheet.

The objects and reasons for insertion of Chapter-IIIB would assume importance in order to better understand the controversy. The same reads as under:

……..For ensuring more effective supervision and management of the monetary and credit system by the Reserve Bank, it is desirable that the Reserve Bank should be enabled to regulate the conditions ……… The Reserve Bank should also be empowered to give any financial institution or institutions directions in respect of matters, in which the Reserve Bank, as the Central Banking institution of the country, may be interfered from the point of view of control over the credit policy. The Reserve Bank's powers in relation to commercial Banks should also be enhanced and extended in certain directions, so as to provide for stricter supervision of the operations and working……..[4] (emphasis added)

The aforesaid makes it clear that the intention of the Parliament to insert the provisions of Chapter-IIIB inter alia is to control and regulate the conditions for acceptance of deposit and to control the credit policy of Non-Banking Finance Companies and the financial institutions.[5] The overarching nature of RBI regulation can be seen through section 45Q:

“The provisions of this Chapter shall have effect notwithstanding anything inconsistent therewith contained in any other law for the time being in force or any instrument having effect by virtue of any such law.]”

This non-obstante clause overrides provision of any other law for the time being in force. Further, besides section 45Q, section 45JA is important as it allows the RBI to direct all or a class of financial institutions and to formulate policy for the same. This will put the burden on RBI to direct MFI NBFCs as it has the wherewithal and legislative competence for the same; not state governments who have experience of only regulating state corporations and money lenders. The Malegam report supports this notion when it forwards the idea that the State is often not the best agency to act as a regulator and this task is best left to an independent regulator[6].

The High Courts of Maharashtra and Gujarat have upheld the primacy of RBI over state regulation on these same grounds, in the cases of Vijay P vs. State of Maharashtra[7] and Sundaram Finance vs. State of Gujarat[8].

The Malegam report records that ideally there should not be any overlap of regulation and regulators for the smooth functioning of financial services. The above point’s buttress this argument and show that legally speaking there cannot be any overlap and the NBFCs must either be governed by List I or II.

[1] Page 49; Para 25.7.

[2] http://www.business-standard.com/india/news/ap-govt-raps-malegam-says-mfi-act-to-stay/422621/; Last visited on 31st January, 2011.

[3] http://www.dnaindia.com/money/report_andhra-pradesh-to-deep-six-malegam-panel-recos_1497525; Last visited on 31st January, 2011.

[4] (2010)51GLR1529

[5] Ibid.

[6] Page no 48; Para no 25.6 (a).

[7] (2005) 128 Comp Cas 196 (Bom)

[8] (2010)51GLR1529

A foreign policy doctrine for India.

Hopes of emulating the success of an ‘Iraqi surge’ in Afghanistan may not have been fully realised. With the US stuck in a quagmire of economic crisis and a perception of loss of power, USA increasingly is looking for a way out. India should have been the traditional go to nation for sharing some of the burdens of the Afghan war, however with Pakistan objecting to even token Indian presence, this seems unlikely.

There is a fair amount of analysis on possible outcomes of USA withdrawal and role of India in such a post-USA Af-Pak world. One of the constants of such analysis has been the certainty of a de-facto Pakistan takeover of Afghanistan. With a return of Taliban and strengthened Pakistani elements, the 60 year old Indian endeavour of settling its western borders would be considerably weakened. A victorious Pakistan would be a recalcitrant negotiator.

Such a gloomy forecast is among others a case of simplification of an unclear narrative. We have frequently looked at the Pakistani and Afghani players as a monolith, with shared interests and common foes. The participants in this story are diverse and engaged in a fight with every other participant, including their supposed allies. Notably the Tehrik-i-Taliban and allies are opposed by the Punjabi governing elite, , national parties, the MQM and partly by the Balochs. Further the areas bordering Afghanistan wherein the Taliban and other extremist agencies are based have not been conclusively lost. Instead FATA, Quetta, Mohammed Agency are frontlines, with Pakistan being the prize.

Let us here for the moment assume Taliban’s victory over Afghanistan, with active Pakistani involvement. Is this really the nightmare situation for India, as has been painted in public discourse. In this author’s personal opinion, partition was the actual nightmare for Indian political and military strategists. All we are facing now are the after-shocks. It reflects negatively that we have yet to come up with a coherent public policy for dealing with results of said nightmare. Lack of communication of Indian foreign policy objectives to the public la the USA is a very significant lacuna on part of Indian administrators. This is so as it is the public which bears the cost for all policies.

In this article we will attempt to look at steps that India may take to turn around a Taliban takeover of af-pak region into a beneficial stand.

In our present context, it is interesting to note that the USA is looking at employing its time tested tactic of dividing a region it cannot hold. The Korean peninsula and Vietnam are prime examples of this approach. It is the US belief that short of an outright victory, a region clearly divided into blue and red is the most effective tactic in stopping a domino effect for the whole region. Vietnam being an example where after US withdrawal, the whole region became communist. A partition of Afghanistan will be of dubious benefit to USA and allies, as it will require continued expenditure of men and political will, to prop up and defend Northern Afghanistan. While this might be an easier task, with a friendlier population, the USA would be stuck in a semi-permanent deployment. From the Indian perspective this would be a very helpful development as;

- The USA will continue to take an active interest in reducing Pakistani radical structures and manpower,

- The focal point of Islamic extremism will continue to be divided between Kashmir and Afghanistan,

- Northern Afghanistan will comprise of friendly elements of the Northern Alliance, which India shares a long standing relationship with.

Though this is a very brief summary of benefits, the logistics would allow India to establish a limited presence on the ground. The challenges for USA would be varied and would require renewed involvement with cold war era players, i.e. the CIS and Russia for setting up such a partition. The one nation which would be the clear beneficiary would be Iran, as it will gain prominence as a stabilising and influencing agent. The challenges for USA would however be gigantic and any partition may at best be a de-facto arrangement.

India needs to formulate a foreign policy doctrine for public consumption which takes into account the history of engagement with Pakistan and ways to deal with the threat of violence centred around the Af-Pak region. An attempt will be made to formulate an example of such a doctrine, later in this discussion.

Monday, January 24, 2011

Creative writing -1

Okay not 2 paragraphs just one; but hey "baby steps". It describes what i was thinking when i was sitting in a airplane recently.

I am lost in my in-flight magazine with only the irritating but strangely hypnotic cabin music to ignore. In time safety instructions are issued, passengers trudge in, disregarding all this i ignore life. The plane nonchalantly trundles along, just another moment in a boring life.

The plane stops, a few seconds of silence and suddenly violence assails my senses, the ferocity of physics drags me from my mental stupor and drowns me in life.

Post script: Is it too early for me to start thinking of sending airmails to Norway.

Heads up

One of my favourite pet theories is the one which talks about dealing with the potential of "bottom of the pyramid". This can encompass everything from markets to social and cultural phenomenon. In India TATA "Nano" is the most visible example of such an attempt. I will try to look at this concept through the traditional idea of importance of credit expansion; in the present context it would mean personal reflections on the Malegam Committe report on "Micro-finance" institutions. I will be handicapped in this analysis with lack of adequate industry experience and will depend primarily on open source information.

I am also trying to write a short opinion piece on why the "Taliban" winning in Afghanistan may be good for India. Also as part of my 10,000 project am trying to dabble in creative writing and will put up my first original work (only 2 paragraphs) of quasi-fiction in some hours.

In reply to Sushant K Singh

A few days ago Acorn posted the following article entry:

"http://acorn.nationalinterest.in/2011/01/18/scrap-offsets-and-foreign-investment-caps/#comments"; For the record i believe that the blog "Acorn" and other affiliated blogs, sites and magazines are an interesting attempt at articulating Indian opinion and any criticism on my part should not be considered to be against the site.

The article talked about the problems with offsets in defence contracts and how recent modifications by the Indian government were a death knell for this policy. Further the author suggested the scrapping of offsets to jump start the Indian private defence industry. I agree to one of his suggestions but am against his conclusions; my dissent is given below.

Dear Mr. Sushant,

This article may be called a good primer for the uninitiated to the topic of ‘Defence Offsets’ (henceforth DFO). However i have a few objections to the conclusions drawn here.

Offsets began as a policy decision in the post 2nd WW era, when western Europe was being re-built and outfitted by USA for the cold war. DFOs helped W-Europe to channel its defence spending to productive national causes. The present article looks at the changes in the DFO policy of India as so many nails to the offset policy coffin. In my personal opinion the situation does not warrant such a bleak outlook. The changes may be considered to be a part of the learning curve for handling technology imports through a private sector initiative. This is an unavoidable situation for India due to the lack of a pvt sector defence capability.

To understand the present situation on DFOs, we need to understand why it introduced in the first place.

India is on an unprecedented expansion of its armed forces. A conservative estimate pegs India’s defence spending by 2022 to be around 100 billion dollars . With the current DFO limit being 30% of a contract value and if the above amount is assumed to be a reasonable figure then domestic manufacturers will get orders worth 21 billion dollars. However the Indian defence offset policy was undeveloped in the area of managing this massive inflow.

To cite a few areas:

1. The idea of multipliers was absent in the offset policy. Hence offsets pertaining to multi-functional display (MFDs) would be on par with offsets dealing with jet engines or AESA radar technology or submarine hull fabrication know-how.

2. Identification of industries which are considered to be priorities for domestic defence industry development. An attempt was made by introducing the concept of ‘Rakhsa Udyog Ratnas’ (RURs), however the same was scuttled due to opposition by the OFBs and other DPSUs.

3. Creation of a national offset policy with a hierarchy of requirements and a clear roadmap laid out for the duration of the Long Term Integrated Perspective Plan (LTIPP).

The author does identify the problem of low FDI as a significant hurdle to building partnerships with foreign players. The easiest solution to this problem would be to increase the FDI limit to at least 49%. However in a deadlock as in the present situation, the Govt may follow the selective route of allowing FDI through the approval instead of an automatic route. This will not require dramatic changes to the present policy along with retaining a measure of control over foreign access to domestic industries.

There are a number of other additions that may be made to the DFO policy including allowing offset trading and increasing the tenure for banking of DFO. However I fail to understand how the author of this article is suggesting that the ‘offset policy’ per se be dismantled due to perceived problems. This is akin to throwing the baby out with the bath water.

Using the example of a Czech aviation firm, he seems to make a case for allowing higher FDI limits. However to make a case for the removal of offsets as a policy, the author will have to provide more inputs as well as examples to make his case. Presently he is only pointing out the inadequacies of Indian DFO policy; to prove his point he will need to argue on-

1. The actual harm caused to the Indian private and-or public sector defence industry due to the offset policy.

2. As a corollary, how imports of defence equipment without a DFO policy will contribute and help the DPSUs and pvt industry build capacity.

I hope that Mr. Sushant or the blog admin for "Acorn" takes the time to respond to these queries.

Subscribe to:

Comments (Atom)